How to cut fees and delays when you send money abroad

Sending money abroad from South Africa can cost more than the quoted fee suggests. Exchange rates, allowances, and compliance checks subtly impact what your recipient finally receives and how long it takes.

Sending money abroad from South Africa can turn into a tiny financial crime scene: one visible fee, mystery exchange rate, and “processing” message, then someone overseas asking why the amount is short.

Anyone watching the rand’s swings during global risk moves already knows timing can be crucial before a transfer even leaves your bank.

South African millennials know that payment apps are fast when local options work efficiently, but cross-border transfers still drag on extra checks, cut-off windows, and intermediary deductions.

Understanding payment option costs helps explain why an international transfer can appear inexpensive upfront and costly once the final amount reaches the recipient.

Where the costs start

The exchange rate can cost more than the transfer fee

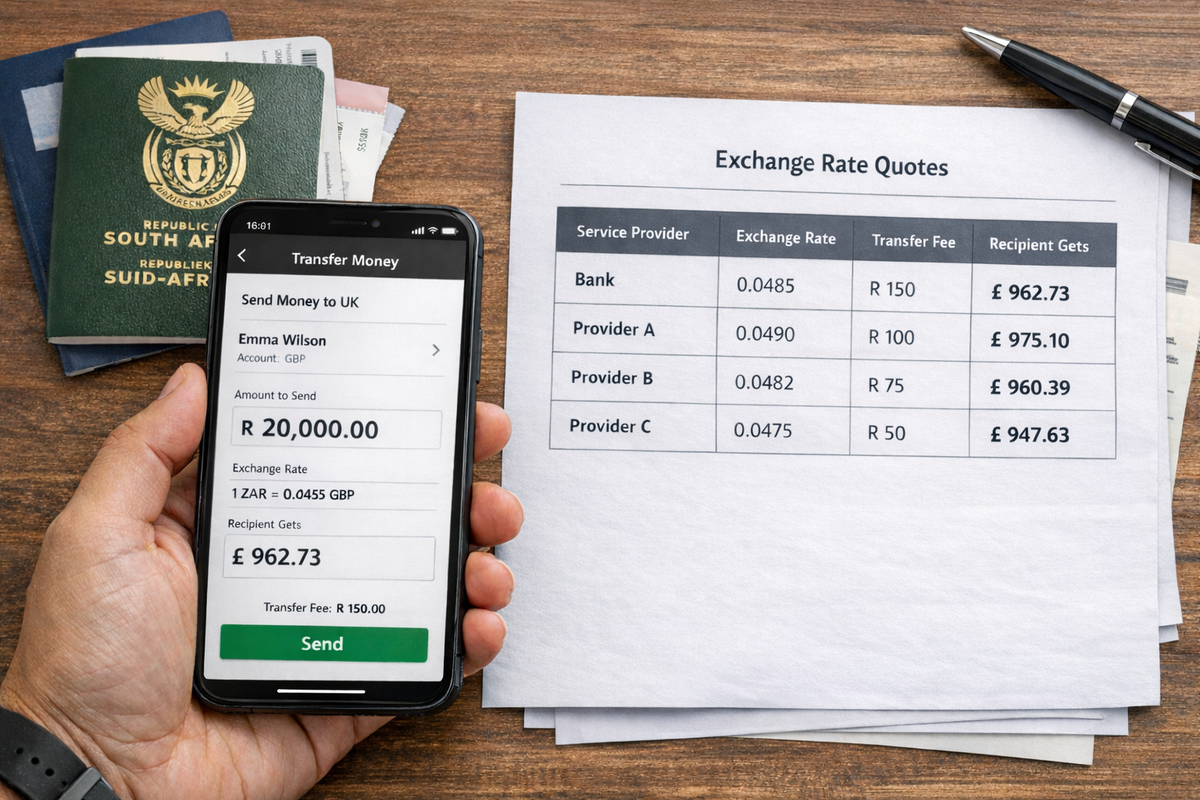

Many people stare at the listed transfer fee and miss the bigger cost: the exchange-rate markup. Two providers can charge similar transfer fees and still produce very different beneficiary amounts because one rate is weaker.

Bank charges are not always the full story

A quote can look cheap at the start, then produce a lower payout once correspondent-bank charges or receiving-bank deductions come off the amount. Some providers show these charges clearly. Others leave more guesswork, which is exactly how people think they sent enough and still come up short.

The beneficiary amount is the number to compare

Price comparisons should start with one question: how much will arrive? The best quote is not the one with the lowest visible fee, but the one that delivers the highest final amount after fees, rate markup, and any transfer-route deductions.

A transfer can look expensive because of bank charges, but the exchange rate can cost more. Compare the amount the recipient receives, not the headline fee on the first screen. One quote can look cheaper while delivering less money at the end.

Why delays happen in South Africa

Banks and providers are checking more than your account balance

South African banks and authorised dealers are not being dramatic when they ask for supporting documents. They work within exchange control rules and anti-money-laundering obligations.

The FIC guidance note confirms a risk-based approach to customer due diligence (CDD), which means that institutions apply checks based on risk and keep records that allow a transaction trail to be reconstructed.

Common delay triggers in local outward payments

- First-time offshore transfer from a new profile

- Missing or inconsistent beneficiary details

- Payment reason does not match the supporting documents

- Source-of-funds questions on larger or unusual transfers

- Tax compliance verification steps for higher-value transfers

- Late-day initiation, which pushes processing into the next bank window

Why “sent” does not always mean “received”

A provider can mark a transfer as sent while the receiving bank or an intermediary bank still has checks pending. Cross-border payments involve handovers, not one straight line.

Fast apps changed local expectations. Cross-border payments still answer to compliance checks, bank cut-off times, and international bank handovers.

South African limits and checks you need to know

South Africa’s outward transfer rules fall under SARB’s Financial Surveillance framework, which sets the thresholds that determine when extra tax verification or formal approval is required.

The R1 million allowance is a real dividing line

Up to R1 million per calendar year can be transferred abroad under the single discretionary allowance without requiring a SARS tax compliance status verification result. Residents aged 18 and older qualify for this allowance.

Above that, tax compliance steps enter the chat

Transfers above the R1 million threshold require tax compliance verification. Authorised dealers verify this through a SARS TCS PIN before processing qualifying transfers. The TCS process is handled through SARS eFiling or SOQS under the “Approval International Transfer” route.

Substantial transfers can face an extra SARB approval layer

If an individual wants to transfer more than R10 million per calendar year for investment purposes, the authorised dealer must submit an application to the Financial Surveillance Department, supported by tax compliance verification.

How to cut fees before you send

Compare by beneficiary payout, not by advertised fee

Open multiple quotes within a short window and compare:

- Total ZAR amount debited

- Exchange rate offered

- Transfer fee

- Any disclosed third-party/correspondent charges

- Estimated beneficiary amount

- Delivery estimate

Ask who pays correspondent-bank charges

Some routes deduct charges along the way. A transfer can leave your account at one amount and arrive short on the other side, and beneficiaries then assume you underpaid. Banks love confusion almost as much as they love forms.

Send during bank hours, not at the edge of the day

Late initiation can push processing into the next local banking cycle or the next destination-country banking cycle. A transfer started earlier offers more daylight for document queries, verification, and corrections.

Use exact beneficiary details

One bad character in an account number, SWIFT/BIC, branch code, name, or reference can trigger manual review. Cross-border payments are hyper allergic to typos.

How to cut delays before they start

Prepare your documents before the first transfer

South African providers could request the following:

- ID document/passport

- Proof of address (usually not older than 3 months0

- Source-of-funds evidence (also the most recent docs)

- Invoice or proof of payment purpose

- Beneficiary details and relationship details (depending on transfer type)

FIC guidance on CDD and record-keeping explains why institutions collect and retain this information.

Use the correct payment reason

Mismatch between the stated purpose and supporting paperwork can slow processing. “Family support,” “tuition,” “travel funds,” and “investment” are not interchangeable labels in a bank workflow.

Track your annual transfers

Allowance usage during the calendar year affects what route your next transfer follows. A person who ignores previous offshore transfers can hit a documentation wall mid-year and blame the app. However, the app did not invent exchange control.

Most transfer delays are not random. Missing documents, unclear payment purpose, typo-heavy beneficiary details, or threshold-related checks create the delay. Preparation cuts waiting time better than angry app-refreshing.

A practical South African sending routine

Use a pre-send checklist every time

- Compare beneficiary payout across at least three quotes

- Check the exchange rate, not only the transfer fee

- Confirm who pays intermediary charges

- Verify beneficiary details character by character

- Confirm your payment reason and documents match

- Check where you are in your annual allowance usage

- Initiate during business hours when possible

- Save quote and confirmation screenshots

Recurring support payments need a system

Rent, tuition, family support, and contractor payments punish people who improvise every month. Re-using a checked beneficiary profile, storing documents, and tracking allowance usage can cut repeat delays and admin loops.

Comments ()