Many South Africans pay avoidable banking fees every month. Here's how to identify it and reduce unnecessary costs.

When reviewing banking fees in South Africa, start with your bank statements, not the bank’s pricing guide. A pricing guide shows what an account can cost. Your statements show what it is costing you. The gap between those two numbers is where unnecessary fees hide.

1. Monthly fees for an account you no longer use properly

Monthly bank fees are easy to ignore because the deductions appear routinely on a bank statement. A bundled account may make sense if you use its benefits. Branch services, extra cards, reward partners, travel perks or frequent transactions can justify a higher fee.

The problem starts when your banking habits change, and the account does not. A person who now uses the app, pays mostly by card and draws less cash may be paying for features no longer used. The question is not whether another bank is cheaper. Check whether the monthly fee still matches the way you bank now.

2. Immediate payment fees used without thought

Fast payments are useful when timing matters. A deposit, urgent family transfer or supplier payment may justify the extra cost. Many payments are not urgent. Standard EFTs, PayShap and bank instant payment services have different fees, limits and processing times, depending on the bank and account.

Before choosing the fastest option, ask whether the money must arrive immediately. A single fee may look small. Repeated throughout the month, it becomes part of a more expensive banking pattern. If you also send money offshore, review international transfer costs separately, because the fee shown upfront is not always the full cost.

3. Cash withdrawal fees chosen for convenience

Cash still has a place in many South African households. Transport, school costs, tips and small traders can still require notes and coins. The fee depends on where and how the cash is withdrawn. ATM, branch and till withdrawals may all be priced differently.

Review three months of withdrawals. Mark every cash fee. Then compare the charges with your bank’s latest pricing guide. You may not need to stop using cash; you may need to stop withdrawing it from the most expensive place.

4. Admin charges hiding in plain sight

Proof of payment requests, paper statements, branch-assisted transactions and older record searches can all attract charges. Some records are necessary for applications, disputes or audits. Others may be available through online banking at no extra cost. Admin fees are usually small, which makes them easy to overlook. Review them alongside payment and cash withdrawal charges.

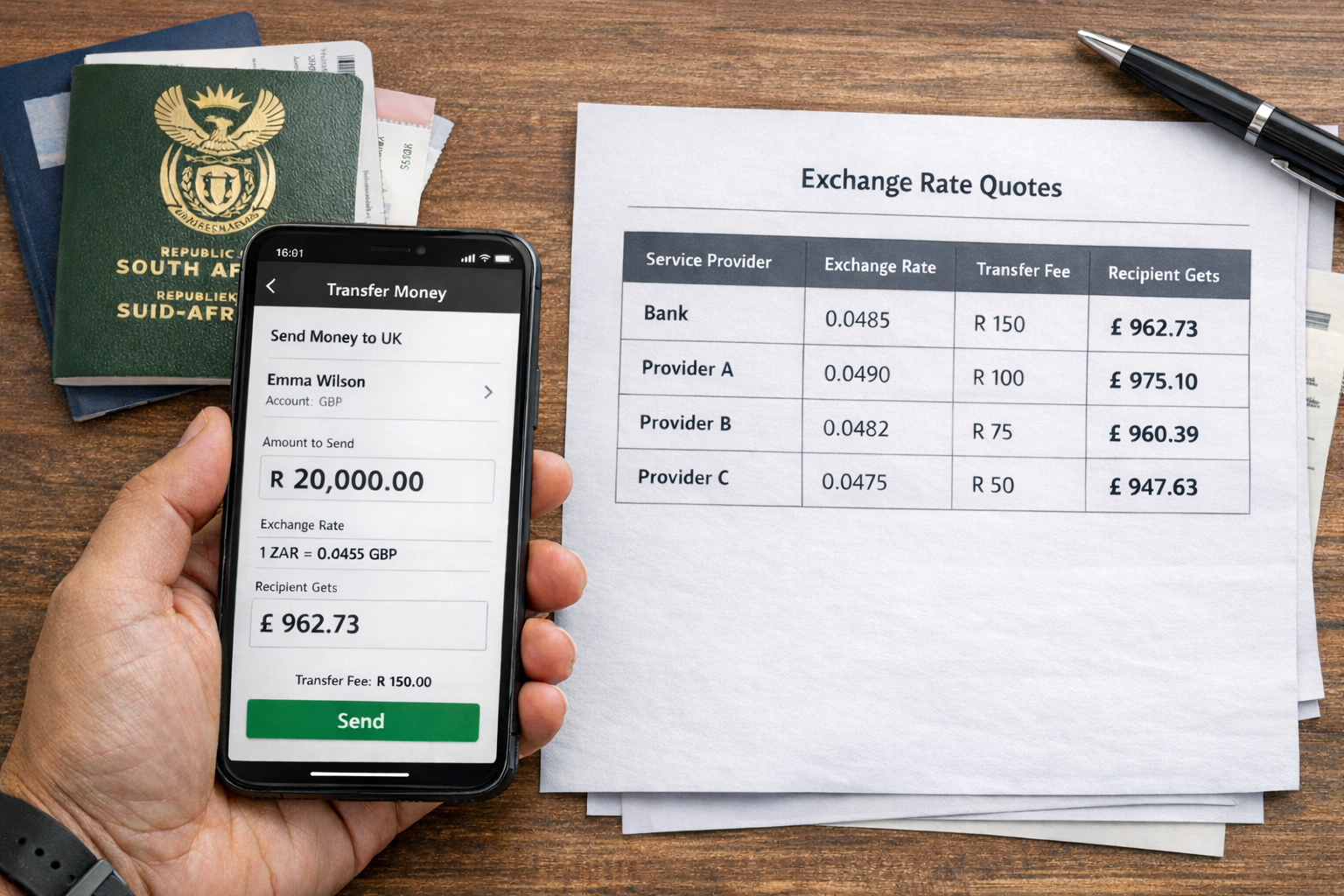

5. Currency conversion costs on foreign payments

Foreign payments cost more than the visible transfer fee. The exchange rate, processing date and possible receiving-bank charges can all affect the final amount. Freelancers, travellers, students, small businesses and families sending money abroad should check the full cost before paying.

Travellers should apply the same thinking to foreign card spending and overseas purchases, where exchange-rate markups can quietly increase costs before the transaction appears on a bank statement.

The same applies to card-linked wallets. Paying with Apple Pay or Google Wallet through South African banks changes the payment method, not the pricing rules behind the card.

The review does not need to end with a new bank account. Start with the fees linked to habits that changed: less cash, fewer branch visits, more card use, more app banking or more international payments. A fee that once made sense can become wasted money when life changes around it. That is where the easiest savings are usually hiding.

A bank fee is only small until it becomes a habit. Review the charges linked to how you used to bank, not how you bank now. If the habit has changed but the fee is still there, that money belongs back in the household.

Comments ()